Some boards run an audit every year, while others stretch it out over two or three years. Other HOAs don’t know when they are supposed to do it; they just wait until something doesn’t feel quite right.

So, how often should your HOA be audited?

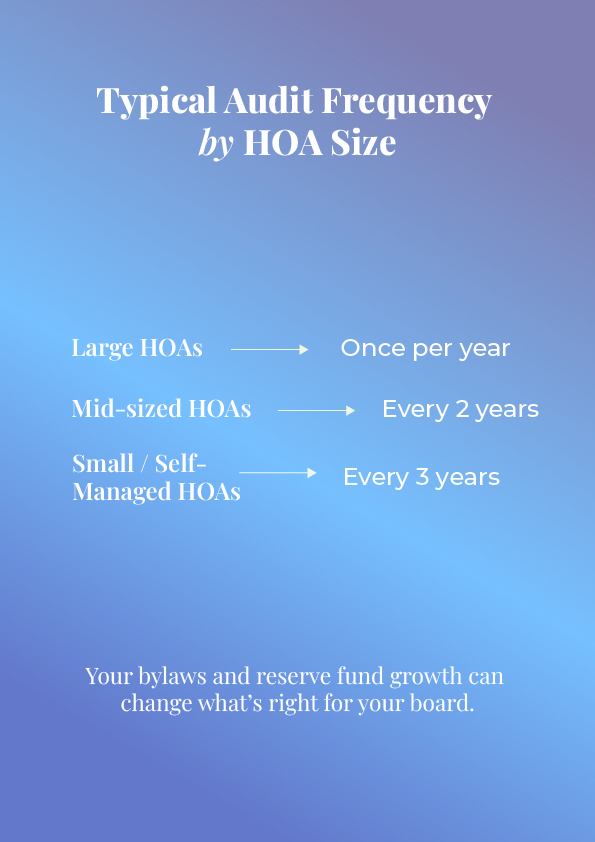

There’s no one-size-fits-all answer, but here’s the usual pattern:

- Larger HOAs get audited once a year

- Mid-sized boards go every two years

- Smaller self-managed HOAs often use a three-year cycle

These are just starting points, and your state law might demand more. Your bylaws set the terms, and your reserve fund could have doubled since your last audit.

SSL looks at the whole picture (not just what’s on paper) and can help give you a clear answer on what makes sense for your situation.

What Should Influence Your Audit Schedule?

As mentioned above, some HOAs tick along fine for years on the same audit cycle, and then one year, everything can change. It could be a larger budget or a few raised eyebrows at the AGM.

The timing of the audits doesn’t have to stay fixed just because it’s always been that way. These are the sorts of changes that can bring that schedule forward:

- Board members step down or rotate out

- Your annual budget looks bigger than last year’s

- You’re planning renovations, such as a new clubhouse roof or resurfacing the pool

- Homeowners start asking for more financial transparency

One HOA we worked with doubled its reserve budget in less than a year. A few major repairs were delayed, and the funds continued to grow. On paper, things looked great, but no one had checked the records in a long time as they were on a 3-year cycle.

Once they hired SSL, we reviewed their accounts and noticed a few issues. One issue was that a contracted payment had been missed, and a deposit had been logged in the wrong place. These were nothing serious, but just enough to cause confusion. We transitioned them to annual audits to provide the board with a clearer view of their financial records and increase their confidence when presenting to homeowners.

Legal Rules That Dictate Frequency

The law sets some audit schedules.

California state requires any HOA with annual revenue exceeding $75,000 to undergo a financial review every year. In Florida, that threshold jumps to $500,000. Other states have their own cutoffs and conditions, which change over time.

That’s just at the state level, and your own HOA’s governing documents might set tighter rules. Some boards are required to conduct a full audit annually, regardless of their budget size or complexity.

This is where things slip. Rules or the board might change, and it’s easy to assume someone else has already checked the legal requirements. This is precisely why you need SSL, as we stay on top of those changes and flag everything that affects your audit timing. If there are any changes to your state law or bylaws, we’ll notify you.