Cash vs. Accrual: What’s the Actual Difference?

Let’s say your HOA sends out dues notices in January. One homeowner pays right away. Another pays in March. A third still hasn’t paid by June.

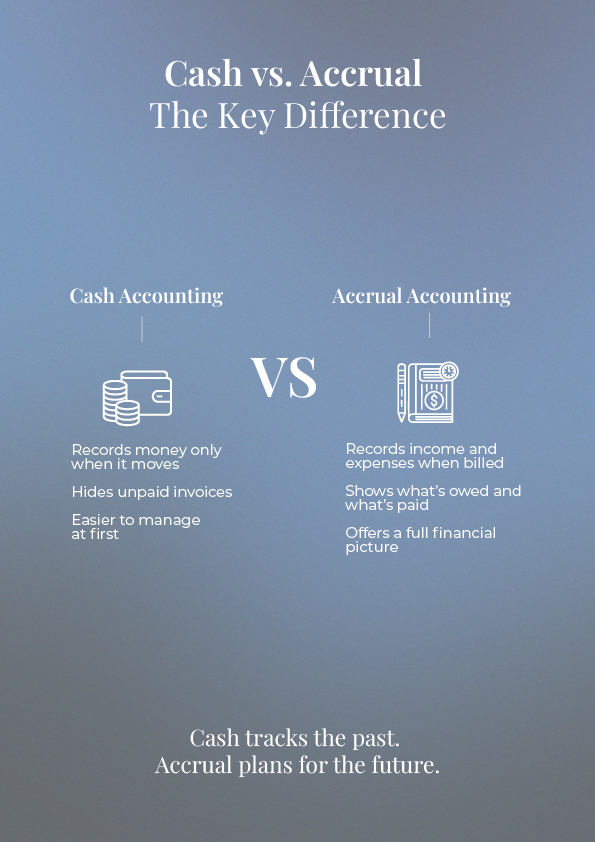

With cash accounting, only the January payment shows up in your January report. The rest don’t appear until the money hits the account. It’s simple. You track money when it moves. But that simplicity creates gaps. Your financial reports won’t show what’s missing.

Accrual accounting records all three dues in January, the month you billed them. You can see what’s owed, what’s paid, and what’s late, even when the money hasn’t hit the bank yet.

This difference affects more than timing. It changes how you:

- Track dues: Cash hides unpaid invoices. Accrual shows them clearly.

- Plan reserves: Accrual gives you a future-facing view. Cash doesn’t.

- Explain shortfalls: Cash creates mystery. Accrual tells a story.

Most HOAs start with cash accounting because it feels easier. But as the community grows, accrual gives the board more clarity and more control.

If the books feel off even when the balance looks fine, this could be why.

Which One Makes More Sense for HOAs?

Most accountants recommend accrual for HOAs, and there’s a good reason for it. Accrual gives boards a clear picture of the financial health of the community, not just the bank balance.

Let’s say your HOA has £20,000 in the bank. Looks fine on paper. But you haven’t paid the landscaping bill, the insurance premium is due next month, and you still need to replace the roof on Building C. In cash accounting, none of that shows up. You see the £20,000 and think you’re in good shape. Accrual shows the whole picture.

That’s why accrual works best for HOAs with long-term projects, reserve planning, or regular service contracts. It helps boards avoid mistakes like:

- Thinking they have a surplus, when they don’t

- Missing unpaid invoices

- Underfunding reserves until it’s too late

Most CPA firms and auditors prefer accrual accounting because it creates a more accurate financial trail. It’s also better for forecasting and budgeting.

Still, not every HOA needs it right away. Smaller, self-managed communities often use cash accounting because it feels easier. If your only expenses are utilities, gardening, and a bit of admin, that might work for a while. But once things scale up, cash accounting starts to hide problems.

That’s when most boards switch. Not by choice. They feel pushed. Money goes missing in the gaps and the reports stop making sense.

Accrual brings those answers back into focus.

What Do the Rules Say

Before choosing between cash and accrual, check the rules. Some HOAs don’t get a choice.

In a few states, law requires accrual accounting once your budget crosses a certain threshold. Some lenders ask for accrual reports before approving loans. Your governing documents might already spell it out, especially if your community was set up with outside financing.

Even if the rules don’t force your hand, other players might. Auditors often prefer accrual. So do reserve study providers and accountants. If your HOA works with any of them, it’s worth asking which method they expect.

Still, some HOAs do have a choice. And that’s where things get interesting.

If no one’s telling you what to do, pick the method that shows the most useful picture of your money. If the cash method hides upcoming bills or gives a false sense of surplus, it may cost you more in the long run. You don’t need to be fancy, just clear.